CC BY-ND

Americans spend about half a trillion dollars per 12 months to charity. This money helps fund services for the homeless, fight disease, operate museums and other organizations that conduct meaningful activities. Some donations, resembling those to support religious communities, are expenses that the The US government couldn’t legally even when it desired to.

This explains why the U.S. tax code encourages giving by granting tax breaks to some donors. When these taxpayers donate, their tax liability is reduced by the charitable deduction.

Overall, this deduction reduces tax revenue tens of billions of dollars per 12 months. Since donations have a social value, the lost tax money could possibly be price it.

Many taxpayers stopped benefiting from this tax relief after President Donald Trump signed the Tax Cuts and Jobs Act into law in late 2017.

This law increased the Flat-rate deductionAs a result, many individuals stopped itemizing and commenced taking the usual deduction as an alternative because they paid less in taxes that way without itemizing.

To 30% of taxpayers itemized their tax returns in 2017in order that they’ll use the deduction for charitable purposes, in accordance with the Internal Revenue Service. But since 2018, only about 10% have individual listings.

For the 30 million taxpayers have stopped providing individual tax breakdownsThe donation deduction was eliminated. They lost an incentive to support a lot of their favorite causes.

I’m a economist who studies charitable activities and public policy. Together with two colleagues, Mark Ottoni-Wilhelm And Xiao-HanI Co-author of a study a have a look at what happened to charitable giving after the Trump-era tax reforms took effect.

Loss of sales

Our study uses data from the University of Michigan Panel study on income dynamicswhich asks families questions over time to look at how their giving behavior modified as tax laws modified. This survey lets us see how the identical families' giving modified after they stopped taking the charitable deduction. This data is on the market every two years. We checked out what happened in 2018 in comparison with 2016.

We found that Americans who stopped itemizing their tax deductions gave less to charity in 2018 than they otherwise would have. On average, these donors who were in a position to reap the benefits of the deduction in 2016 gave nearly $1,000 less in 2018 because they missed out on the tax break.

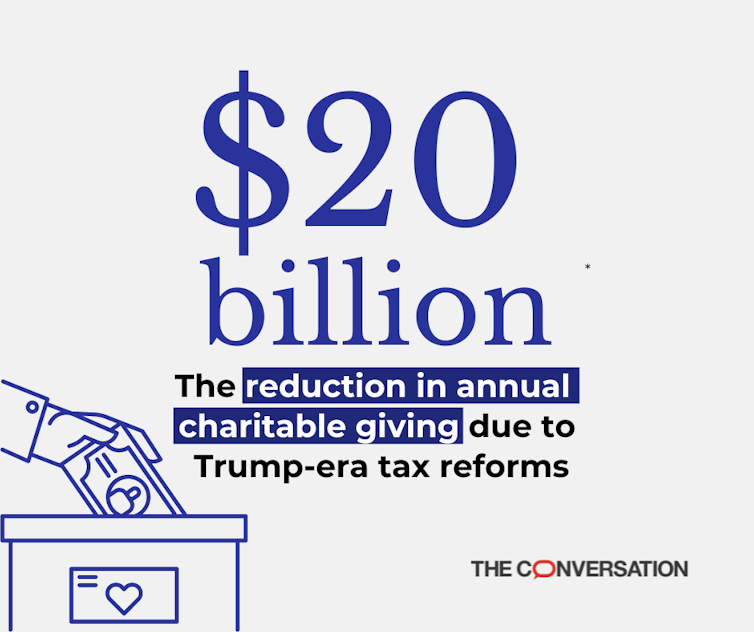

Overall, we estimate that the 2017 tax package reduced individual giving the next 12 months by about $20 billion in comparison with what would have happened had the law not been enacted – about 5% of all giving.

Overall, giving fell from $528 billion the 12 months before to $523 billion in 2018, measured in 2023 inflation-adjusted dollars, in accordance with the Giving USA Foundation's annual report, prepared in partnership with Indiana University's Lilly Family School of Philanthropy. They fell again in 2019, then rose in 2020 and 2021 before falling again in 2022 and 2023, to $557 billion.

Giving from individuals fell by $2 billion after similar fluctuations, reaching $374.4 billion in 2023, in comparison with $376.4 billion six years earlier in 2017. Giving from foundations and corporations increased in the course of the same six years. Bequests from deceased individuals declined – a mirrored image of Impact of other changes within the Tax Cuts and Jobs Act.

To be clear, donations often increase from 12 months to 12 months – especially when the economy is doing well, as has generally been the case in the last yearsIf tax laws had not modified, we might have expected a rise in donations, especially from individual donors, after 2017.

New opportunity to encourage donations through tax law

The donation deduction encourages donations, but costs the state money in the shape of lost tax revenue. Economists and politicians have long been asking themselves whether the trade-off is smart. We imagine our study provides clear evidence that tax law can encourage charitable giving.

Congress can have a brand new opportunity to expand tax incentives for charitable giving in 2025, before many Tax Cuts and Jobs Act Provisions expire in 2026.

Some legislators are already try to extend incentives for donors who don’t itemize their tax returns. But it will not be clear whether they are going to prevail once the talk becomes more heated.

image credit : theconversation.com